Different countries follow different taxation systems

- Countries like India, Australia, and the UK follow a residence-based tax system.

- The USA follows a citizenship-based tax system.

- Countries such as Singapore, Malaysia, and Thailand follow a territorial tax system

- Countries like The Bahamas, The Cayman Islands, and Bahrain do not levy income tax.

- Middle Eastern countries (UAE, Kuwait, Saudi Arabia, Oman, etc.) also do not levy income tax on individuals.

Let’s understand this in detail:

In a residence-based tax system, a country taxes individuals on their global income. This means that if you live and work in a country that follows residence-based taxation, you must report and pay taxes on income earned both domestically and overseas.

In a citizenship-based tax system, a country taxes its citizens on their global income, regardless of where they live. This means that even if you live and work abroad, you may still be required to report and pay taxes in your home country.

For example, a US citizen or Green Card holder must file and potentially pay taxes in the USA even if they live and work in India for the entire year.

This creates a situation where a person becomes a tax resident of two countries, India and the USA. The person becomes a tax resident of India under the residence-based system (because they stayed in India for more than 183 days) and also a tax resident of the USA under the citizenship-based system.

In such cases of dual residency, the individual takes help from the tie-breaker test prescribed in Article 4 (Resident) of the DTAA.

Why is the tie-breaker test important in cases of dual residency?

The tie-breaker test helps determine which country will treat the individual as a resident for treaty purposes.

Based on this outcome, the person knows where to file the Income Tax Return (ITR) as a resident and where to file as a non-resident.

Since the Double Taxation Relief rules provide that Foreign Tax Credit (FTC) can be claimed only in the country where the person is treated as a tax resident, the tie-breaker test becomes essential to avoid double taxation and ensure correct tax compliance.

Almost all tax treaties provide a tie-breaker test to resolve situations where an individual may be considered a resident of two countries.

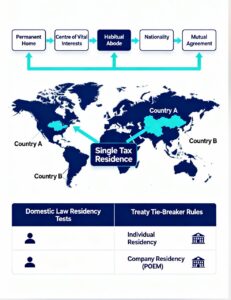

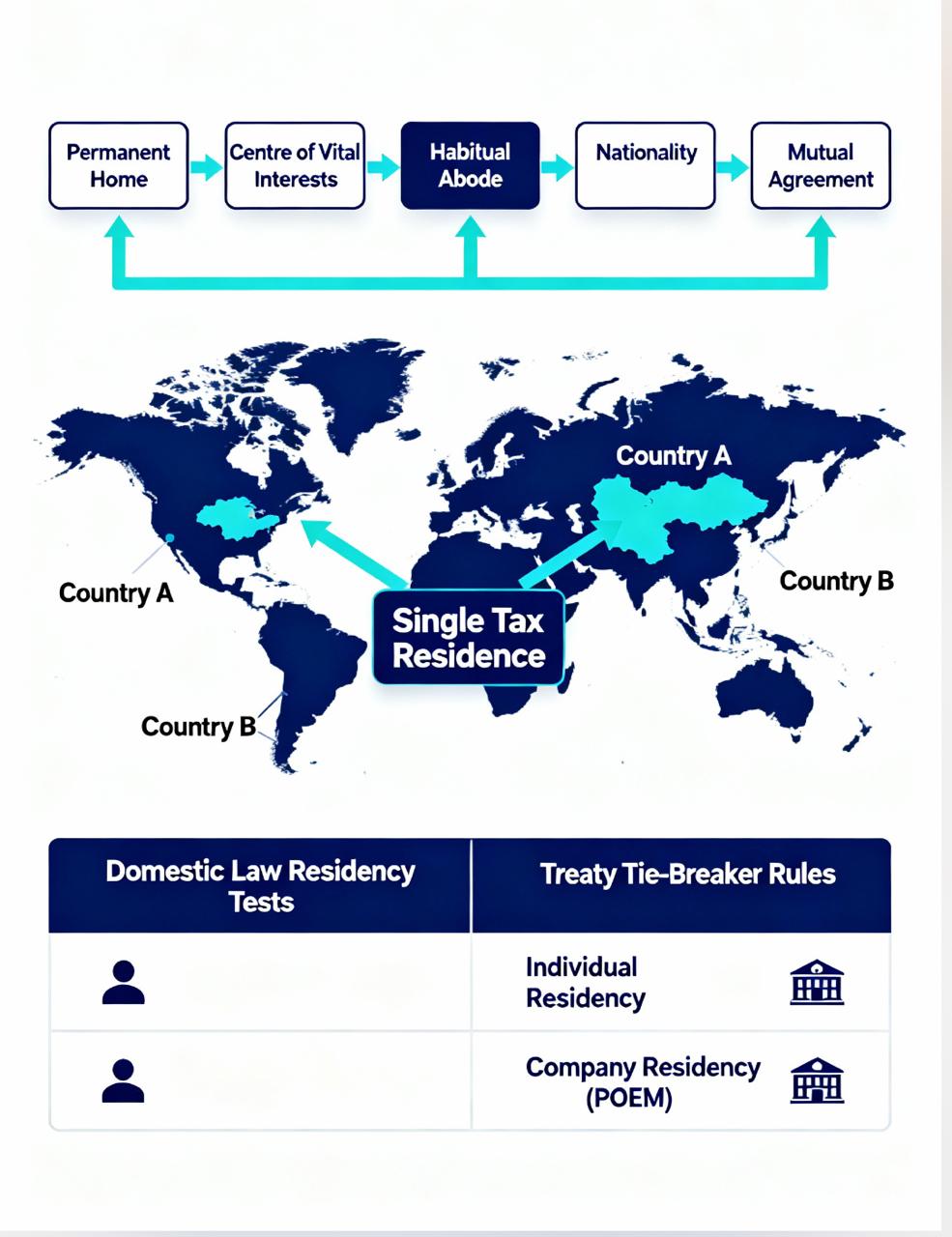

Article 4 of the India–USA Tax Treaty states that where an individual is a resident of both India and the USA, their residential status shall be determined as follows, in the order provided:

- Permanent home: He shall be deemed to be a resident of the country where he has a permanent home available to him.

- Center of vital interests: If he has a permanent home available to him in both countries, he shall be deemed to be a resident only of the country with which his personal and economic relations are closer.

- Habitual Abode: If his center of vital interests cannot be determined, or he does not have a permanent home in either country, he shall be deemed to be a resident only of the state in which he has a habitual abode.

- Nationality: If he has a habitual abode in both countries or in neither of them, he shall be deemed to be a resident only of the country of which he is a national/citizen.

- Competent Authority Mutual Agreement: If he is a national/citizen of both countries or of neither of them, the competent authorities of the two countries shall endeavor to settle the question by mutual agreement procedures (MAP)

Interpretation of Permanent Home and Centre of Vital Interest as per OECD

In respect of the first test, the OECD Commentary states that a person is said to have a permanent home in that country in which he owns or possesses a home which he has arranged and retained for his permanent use.

Where it is evident that the person’s stay at a particular place is for a short duration, it should not be considered his permanent home. It does not matter whether the residential premises are owned or rented by the person.

With regard to the centre of vital interests, to ascertain which of the two countries an individual’s personal and economic interests are closer, regard must be had to family and social relations, occupations, political, cultural or other activities, place of business, place from which property is administered, etc.

Tie-breaker test is applied only in the case of individuals.

Let’s understand this with a situation-based example

Ms. Lily has been living in India for the past 5 years in an ashram as a Sadhvi. Her stay in the ashram is entirely at the pleasure of the ashram; she does not have any other abode in India. She has a home in San Francisco, California, where her parents continue to reside, and she goes back home frequently. She continues to hold a California driver’s license and is also registered to vote in California. She has paid income taxes in the U.S. and in the State of California for a long time. Her entire family resides in California and the vast majority of her economic assets are also in the United States. She receives some sustenance income from the ashram for carrying out social services, which she saves in her bank account in India. She earns some interest income from the bank account, and her total earning in India is little more than the minimum exemption threshold.

While at the ashram, Lily occasionally teaches history and philosophy to visitors at the ashram, for which she receives remuneration.

Note: She holds a Green Card in the US and is treated as a tax resident in the US.

Based on these facts answer the following questions:

(a) Explain the test of tax residence of individuals in India as per Income-tax Act, 1961.

(b) Advise Lily on filing a return of income in India. Discuss how you would apply the tie-breaker test for residence under the India–USA DTAA in Lily’s situation.

Answer (a) Under the Income-tax Act, 1961 an individual is considered to be a resident in a financial year if either of the two conditions are satisfied:

- He/she is in India in the financial year for a period of 182 days or more; or

- He/she is in India for a period of 60 days or more during the financial year and 365 days or more during 4 years immediately preceding the financial year.

However, the period of ‘60 days’ shall be extended to ‘182 days’ in case of an individual:

- Being an Indian citizen who leaves India in any financial year as a member of the crew of an Indian ship, or for the purpose of employment outside India; and

- Being an Indian citizen or a Person of Indian Origin (PIO) who comes on a visit to India during the financial year.

Answer (b) Lily is admittedly a tax resident of the USA. She also qualifies the residence test under the Income-tax Act, 1961 as she crosses the threshold of 182 days in a financial year in India. Therefore, Lily qualifies as a tax resident in both countries.

If Lily is a tax resident of India, she has to file a return of income and pay income tax in India, as her global income crosses the minimum threshold below which no income tax is payable.

Since Lily has dual residence in India and the USA, as per the India–USA DTAA, a tie-breaker test is applied as follows:

The ashram in India cannot be regarded as Lily’s permanent home, as she stays there at the pleasure of the ashram and cannot be considered as occupying the space as a right. She has her permanent home in the USA where her parents reside. Even if she arguably had permanent homes in both countries, her centre of vital interests continues to be in the USA. This is because of factors such as the presence of her family in the US, majority of her financial assets in the US, her voter registration in the US, and her possession of a US driver’s licence. These factors indicate that she has closer economic and personal interests in the USA.

Therefore, the first test breaks in favour of the USA. No other test would be applicable. Lily would be considered a US resident under the treaty.

Therefore, while she would be required to file a return of income in India due to her India-sourced income, she should declare herself as a non-resident.

Conclusion

The tie-breaker test is a critical mechanism under Article 4 of the DTAA to resolve dual tax residency. It ensures clarity on which country will treat the individual as a tax resident, thereby preventing double taxation and enabling correct claiming of Foreign Tax Credit. Applying the structured tests—permanent home, centre of vital interests, habitual abode, nationality, and finally competent authority—ensures a fair and consistent outcome.

Author: CA Pawan Kumar, Head of Taxation.

Linkedin Profile: https://www.linkedin.com/in/ca-pawan-kumar-86636252/?originalSubdomain=in

■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■■

© Copyright CA Shastra. No part can be copied or circulated without the permission of CA Shastra.